Bentley Systems: From a Little Company to a Big Vision

How a Family Startup Transformed into an Industry Powerhouse, and Still Refuses to Compromise on Its Aspirations

Over the past four decades, Bentley Systems has evolved from a small, family-owned startup into a publicly traded leader in infrastructure software. Along the way, it has navigated a 40-year rivalry with Autodesk, pursued numerous acquisitions to fuel its digital twin vision, spearheaded innovative pricing strategies, and even survived a dramatic takeover attempt that ultimately fell apart. As Bentley continues refining its product suite and incorporating new technologies, its trajectory points to an even more expansive role in the future of design, construction, and asset management.

Humble Beginnings

Despite being a major publicly traded firm today, Bentley Systems had modest origins. In 1984, five brothers founded the company in Exton, Pennsylvania, a suburban town of roughly 6,000 residents located about an hour outside of Philadelphia. Early on, Bentley’s portfolio consisted solely of MicroStation, its flagship CAD software that remains a cornerstone of many engineering workflows.

Over the next 40 years, Bentley grew substantially. Today, it boasts more than 5,000 employees and over 30 products, having gone public in 2020 to secure the capital needed to capture the entire infrastructure workflow. Currently, Bentley’s core offerings support three major steps of that value chain:

MicroStation (Engineering modeling, comparable to AutoCAD)

ProjectWise (Project delivery, comparable to Procore)

AssetWise (Operations and maintenance, comparable to IBM Maximo)

Each of these solution families has been expanded through an array of acquisitions, all of which integrate into the iTwin Platform (as shown above)—the central digital twin solution serving as a single source of truth. The iTwin Platform consolidates data from design to project management to asset oversight, enabling users at any point to see the infrastructure’s entire history. Not only does iTwin work with Bentley’s internal workflows, it also integrates with key third-party solutions such as ArcGIS, AutoCAD, and Revit—a topic we’ll explore in more detail later. To accelerate this digital-twin ecosystem, Bentley launched both the iTwin Partner Program and the $100 million iTwin Ventures CVC fund, each aimed at spurring new integrations and industry adoption of digital-twin technology.

A Fierce Rivalry

Around the same time Bentley was taking root, another company was shaping the CAD landscape in Silicon Valley: Autodesk. Its AutoCAD product competed directly with MicroStation, establishing a 40-year rivalry. Autodesk enjoyed the advantage of its Bay Area location, which helped it quickly solidify itself as the go-to CAD solution. Bentley trailed close behind.

Though both companies started on similar footing, their product strategies soon diverged. Autodesk maintained a broad, horizontal approach, offering solutions across engineering and architecture (e.g., Revit). Meanwhile, Bentley went deep into vertical niches, focusing on utilities, heavy civil, and industrial sectors. In essence, Autodesk is the “catch-all” for general design, whereas Bentley dominates specialized verticals that demand more tailored features. Today, both are placing significant bets on the role of AI in the future of design. Bentley mentioned AI 19 times in its latest annual report, with Autodesk close behind at 14.

Bentley’s 2020 IPO solidified its place among well-established competitors in a crowded market. Alongside Autodesk, firms like Trimble, Procore, Dassault Systèmes, and Nemetschek all vie to capture a slice of the market. Despite not leading in total revenue, Bentley’s 10% YoY growth keeps pace with rivals. With a market capitalization around $13 billion, there may be considerable upside if it can execute its ambitious strategies.

Looking Forward: Bentley’s Growth Strategy

To hold its own against industry giants, Bentley needs a well-defined, sharply executed plan. According to the company, three growth strategies stand out:

Penetrate further into enterprise accounts

Expand into the SMB market

Advance the digital twin vision

Below, we delve into Bentley’s approach in these areas and examine how it’s driving each initiative forward.

Betting Big on Digital Twin and Data Freedom

Bentley’s 2024 10-K annual report makes its long-term bet on “digital twins” very clear. The company argues that infrastructure data, spanning BIM, CAD, and GIS, remains siloed, preventing the industry from reaching its full potential. In Bentley’s view, the future lies in unifying all data under a single digital twin platform. By placing iTwin at the center of this next wave, Bentley seeks to “consolidate separate market spaces as well as enable new use cases that were not possible or practical with previous technologies”.

Critical to this vision is the promise of data freedom—where openness and completeness allow customers to access and move their own data with no constraints or lock-in. Bentley strives for open-source compatibility and accessible APIs, ensuring users can readily import and export data across various tools, both internal and external. The end goal is holistic data completeness: giving infrastructure context from start to finish, a concept that underlies Bentley’s acquisitions strategy.

Acquisition Acceleration

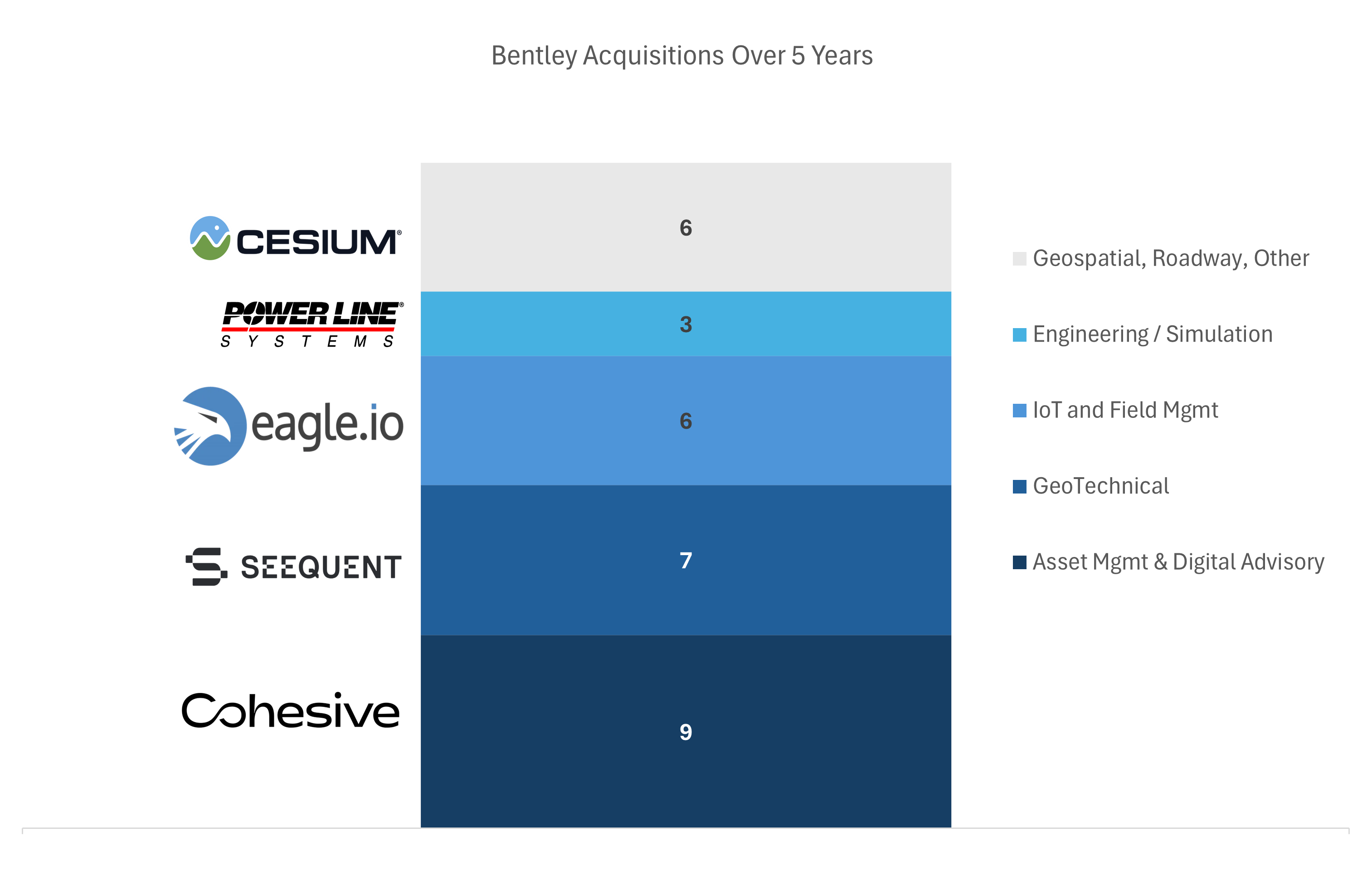

Bentley’s vision relies heavily on inorganic growth—“buy anything and everything” might be only a slight exaggeration. Since its 2020 IPO, the company has completed around 25 acquisitions, spending over $2.3 billion. In the same period, Autodesk made 11 acquisitions, with Trimble at 6. Much of Bentley’s M&A is fueled by fresh capital from its IPO. As a point of comparison, Procore, another recently public AEC player, acquired just two companies the year after its IPO, while Bentley snapped up 13. Bentley categorizes its acquisitions into two groups: large-scale “platform” acquisitions, which significantly expand Bentley’s broader product ecosystem (such as Seequent or Power Line Systems), and smaller, targeted “programmatic” acquisitions, designed primarily to fill specific feature gaps or enhance existing product functionality.

Bentley also leverages acquisitions to expand its international footprint, with a particular focus on EMEA and APAC. These regions collectively contributed around 47% of the company’s total revenue in 2024. Over the last five years, nearly a quarter of Bentley’s acquisitions have been based in Europe or Oceania, providing not only new software capabilities but also valuable local brand recognition and human capital.

What exactly is Bentley seeking through this aggressive M&A approach? The overarching aim is to shore up five core categories, each vital to the iTwin platform vision:

Digital Advisory and Asset Management:

Over the past five years, a significant portion of Bentley Systems’ acquisitions has centered on digital advisory & asset management, a cornerstone of its digital twin vision. By targeting industries like utilities, industrial, and energy—which tend to lag in technology adoption—Bentley not only generates recurring service revenue but also locks in these customers early, cementing them onto the iTwin Platform at the very beginning of their digital journey. Much like how Autodesk secured loyalty by offering AutoCAD to university students, Bentley aims to foster long-term platform adoption by guiding businesses through their initial start to digitalization.

This approach also extends Bentley’s reach into asset management. By helping clients gather and analyze detailed asset data, Bentley positions them to manage projects holistically within iTwin, rather than limiting focus to design and construction alone. The 2020 acquisition of Atlanta-based Cohesive Solutions launched Bentley’s advisory subsidiary, The Cohesive Companies. Several IBM Maximo implementation firms and Bentley’s own AssetWise Services soon joined the fold, creating a unified force dedicated to scaling iTwin-driven asset tracking worldwide. In essence, Bentley is bundling digital consulting with software solutions to accelerate the global adoption of its platform.

IoT and Artificial Intelligence:

In 2021, Bentley acquired Vista Data Vision and Sensemetrics, both specializing in IoT sensor management and monitoring. It followed up in 2023 with the purchase of Eagle.io, a cloud-based industrial IoT data management platform. Each of these deals further strengthens Bentley’s ability to offer real-time asset oversight, integrating critical IoT data directly into the iTwin ecosystem. The strategy is straightforward: the more effectively customers can track their infrastructure, the more indispensable iTwin becomes.

Beyond immediate IoT applications, Bentley sees these moves as essential to its larger artificial intelligence ambitions. With comprehensive data flowing into iTwin, Bentley will be well-positioned to win the AI race. In a telling sign, the company appointed James Lee as COO in January 2025. Lee previously led Google Cloud’s AI initiatives as a General Manager. This executive hire signals Bentley’s commitment to pioneering AI in infrastructure management.

Geotechnical and Geospatial:

Bentley’s drive to provide deeper context for digital twins has led to some of the largest acquisitions in the AEC sector. In 2021, it purchased Seequent, a 3D geoscience modeling firm, for $1.05 billion, followed by the 2024 buyout of Cesium GS, a 3D geospatial solution provider. These deals highlight Bentley’s belief that a true digital twin must account not only for the asset itself but also for the ground beneath it and the broader environment around it. By incorporating geotechnical and geospatial data, Bentley aims to deliver a holistic view—enabling infrastructure owners and operators to understand precisely where an asset sits and what conditions it must withstand.

Engineering and Simulation:

While Bentley has expanded well beyond its roots, engineering and simulation remain integral to its DNA. The 2022 acquisition of PowerLine Systems (PLS) illustrates this focus: with an estimated 90% market share in transmission line design, PLS gives Bentley a commanding presence in yet another niche. By securing top-tier solutions in specialized engineering sectors, Bentley fortifies its core competencies and maintains a strong competitive stance against Autodesk’s broader, more generalist offerings.

Pricing Strategy

Bentley is betting big on the future of digital twins and driving this vision through acquisitions but how are they addressing their growth strategies into enterprise and SMB market? Well both market segments are being targeting primarily through pricing and packaging strategies. Bentley has enlisted two offerings to address these market segments:

E365 Consumption-Based Pricing (Enterprise)

Virtuosity Offering (SMB)

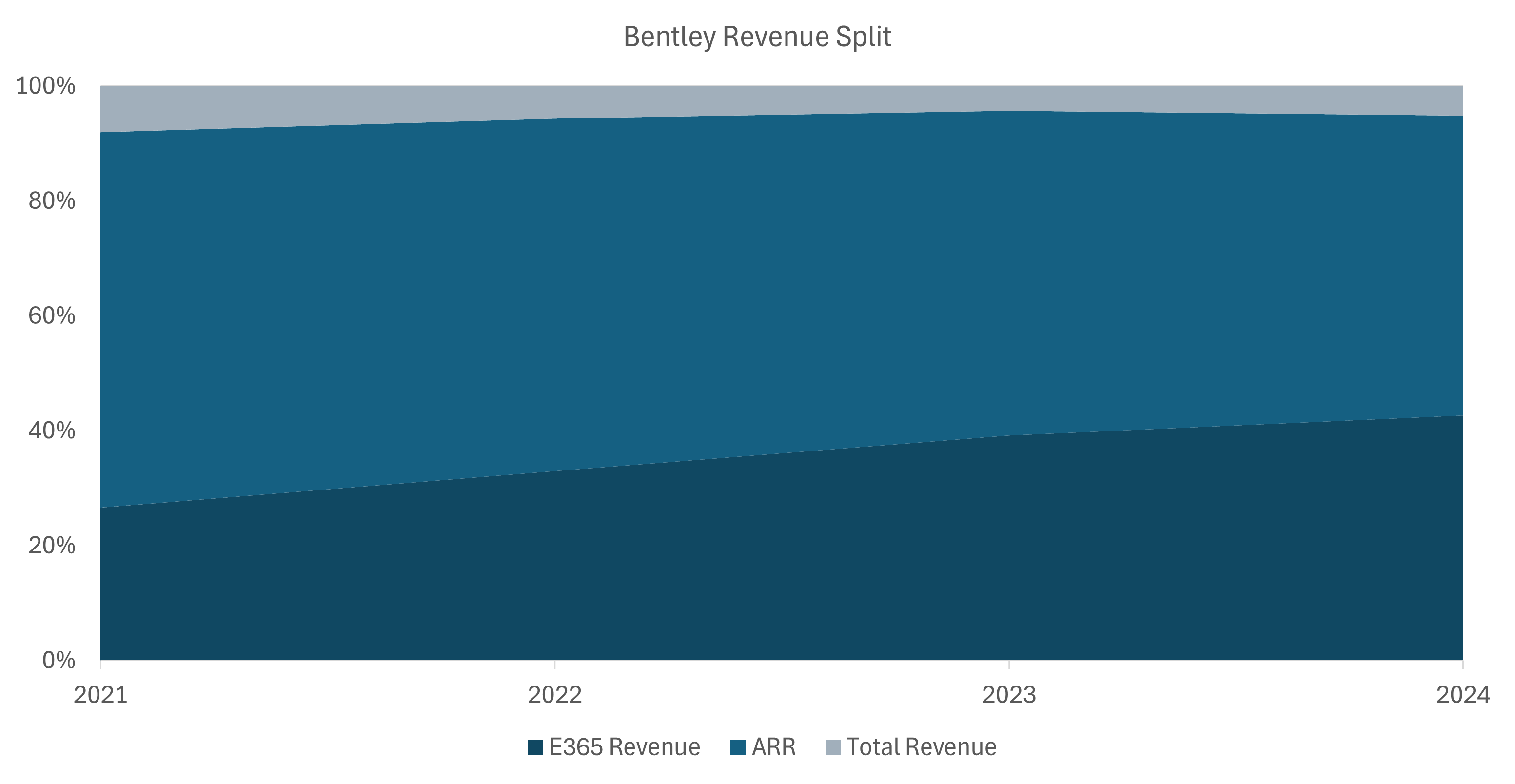

E365 is a subscription-based pricing model that allows enterprise customers unlimited access to Bentley’s entire cloud software suite without per-user license restrictions. Pricing is based on daily consumption, with usage tracked continuously and billed periodically (typically monthly or annually). Enterprises can freely explore new products without upfront commitments, facilitating broader adoption and product stickiness through a flexible, product-led growth strategy.

Bentley launched the E365 program in 2020 and now encompasses 45% of their total ARR (up 16% from first year). Bentley ultimately aims to transition all enterprise clients to E365.

The Virtuosity offering is specifically designed for SMB customer adoption. This program is a “low touch” self-service adoption offering primarily driven through their e-store. This model is cost-effective and simple for a small customer to purchase Bentley software, onboard, and begin utilizing without assistance. The offering comes with a set amount of training and requires no contract. This allows Bentley to create an affordable upfront cost for small businesses by reducing the sales cycle, implementation costs, and operating costs associated with customer acquisition.

The Failed Takeover: A Cultural Mismatch

In early 2024, Bentley Systems was in advanced talks to be acquired by Schneider Electric, a French conglomerate that saw Bentley’s software focus as complementary to its hardware and automation expertise. For Schneider, the deal promised an end-to-end offering across multiple verticals (notably water), plus a strong push toward software subscription revenue to impress shareholders. Bentley revenue is about 88% subscription whereas, Schneider’s is only 8%.

When the deal fell through in May 2024, both companies cited a mutual termination. However, cultural differences appear to have played a major role: Schneider is a multinational French firm, while Bentley remains under family ownership. For the Bentley brothers, surrendering control proved to be a nonstarter, particularly due to concerns about the significant international shift in company culture that would accompany such a change. Notably, this wasn’t Bentley’s first interaction with a big suitor. In 2020, it also explored a sale to Siemens before opting instead for an IPO. Critics speculate that Bentley’s owners want a lucrative exit but balk at relinquishing family control when the time comes to finalize a deal.

Forging the Future of Infrastructure

Bentley Systems has set bold ambitions for its future, backing them with a focused strategy and steady investment. With each acquisition strategically reinforcing its comprehensive digital-twin vision, Bentley continues to build a robust and integrated product ecosystem. By maintaining its commitment to open data, flexible pricing models, and pioneering new technologies like AI, this family-founded company is poised to remain a defining force in infrastructure software—shaping not just its own future, but the industry as a whole.

Super interesting read - thanks! The only important aspect I would add is that Bentley Systems has a long-term cooperation with Siemens (PlantSight). Siemens holds at least 10% of Bentley stock. If anyone would acquire Bentley it would surely be Siemens, which is pushing into software and AI (acqusition of Altair Engineering).